SPACEX AT $1.77 TRILLION: AN EXCEPTIONAL COMPANY AT AN EXTRAORDINARY PRICE

SPACEX OFFERS INVESTORS STARLINK’S PROVEN ECONOMICS, STARSHIP’S TRANSFORMATIVE POTENTIAL AND XAI’S ENORMOUS OPTIONALITY. YET AT AN ISSUE PRICE OF $135 PER SHARE, MUCH OF THAT EXTRAORDINARY FUTURE APPEARS TO HAVE BEEN PRICED IN ALREADY.

Text by Max

Disclaimer: This article is an independent analytical assessment provided for informational purposes. It does not constitute personalised investment advice or a recommendation to buy, hold or sell any security.

Published 12 June 2026

SpaceX is not an ordinary initial public offering.

The company has transformed access to orbit through reusable rockets, built the world’s largest satellite broadband network and become an indispensable contractor to NASA and the United States military. Its long-term ambitions extend far beyond launch services and telecommunications. They include direct-to-mobile connectivity, fully reusable heavy-lift rockets, artificial intelligence infrastructure in orbit and, ultimately, permanent human settlement beyond Earth.

It is therefore tempting to frame the investment debate as a contest between those who believe in SpaceX and those who do not.

That is the wrong distinction.

A company can be technologically exceptional while its shares are priced too aggressively. Conversely, a demanding valuation does not imply that the underlying company is fraudulent, unimportant or destined to fail.

The central question is simpler:

HOW MUCH FUTURE SUCCESS MUST SPACEX DELIVER TO JUSTIFY A VALUATION OF APPROXIMATELY $1.77 TRILLION?

The answer is that success alone may not be enough. At $135 per share, SpaceX must deliver several extraordinary outcomes at the same time, and do so before capital expenditure, competition, dilution and governance risks consume too much of the value created.

THE LARGEST IPO IN HISTORY

SpaceX sold approximately 555.6 million shares at $135 each, raising about $75 billion before expenses. The offering valued the company at approximately $1.77 trillion on a fully diluted basis, making it one of the world’s most valuable listed companies from its first day of trading.[1]

The scale of the offering is unprecedented, but the valuation is even more remarkable when compared with the company’s present financial results.

SpaceX reported consolidated revenue of $18.67 billion in 2025, an increase of 33 per cent from the previous year. It nevertheless recorded an operating loss of approximately $2.59 billion and a net loss of $4.94 billion.[2]

At the IPO price, investors are therefore paying roughly:

94 times trailing annual revenue

approximately 269 times consolidated adjusted EBITDA

no meaningful price-to-earnings multiple, because the company is loss-making

These multiples do not prove that the shares must fall. Conventional valuation ratios have often failed to capture businesses undergoing genuine technological transformation.

They do, however, reveal how little of the valuation can be explained by SpaceX’s current earnings. Most of the price represents expectations about economic value that has not yet been created.

NET LOSSES ARE NOT THE SAME AS CASH BURN

SpaceX’s reported losses require careful interpretation.

A net loss is an accounting result. It is not the same as negative operating cash flow. In fact, SpaceX generated approximately $6.79 billion in cash from operating activities in 2025.

The pressure appears further down the cash-flow statement.

Capital expenditure reached approximately $20.74 billion during the year. Subtracting capital expenditure from operating cash flow produces a simplified free-cash-flow deficit of almost $14 billion.

The pattern intensified in the first quarter of 2026:

This distinction matters.

SpaceX is not a company without a viable operating business. Its established activities generate cash. The difficulty is that its expansion into artificial intelligence, Starship and satellite infrastructure currently consumes considerably more cash than those operations produce.[3]

The IPO gives SpaceX an enormous capital reserve. The company indicated that the net proceeds would be used to expand AI computing infrastructure, launch facilities, launch vehicles and satellite constellations.

Raising $75 billion demonstrates extraordinary investor demand. It does not demonstrate that the projects financed by that money will generate attractive returns.

Investors must assess whether each additional dollar spent is widening a durable competitive advantage or simply financing increasingly ambitious experiments.

THREE VERY DIFFERENT COMPANIES UNDER ONE SHARE PRICE

The present SpaceX group is best understood as three businesses with very different economics.

1. CONNECTIVITY: STARLINK IS THE FINANCIAL ENGINE

The Connectivity segment, primarily Starlink, generated:

$11.39 billion in revenue during 2025

$4.42 billion in operating profit

$7.17 billion in segment adjusted EBITDA

Revenue grew by almost 50 per cent during the year, while operating profit more than doubled. By March 2026, Starlink had approximately 10.3 million subscribers and around 9,600 satellites in orbit.[2]

This is the strongest part of the investment case.

Starlink combines rapid growth with an infrastructure advantage that would be extraordinarily difficult and expensive to reproduce. SpaceX designs and manufactures the satellites, launches them on its own rockets and operates the network. Vertical integration gives the company control over costs, capacity and deployment schedules.

Starlink should not, however, be mistaken for an almost costless software platform.

Satellites have finite operational lives and must continually be replaced. Network capacity requires repeated launches, new ground infrastructure, user terminals, spectrum rights and regulatory approval across many jurisdictions.

Average monthly revenue per Starlink subscriber also fell from approximately $99 in 2023 to $81 in 2025 and $66 during the first quarter of 2026. Much of this decline reflects international expansion and lower-priced services in less affluent markets. That may be economically rational, but it demonstrates that subscriber growth does not translate automatically into equivalent revenue growth.

Starlink is a highly attractive business. It is not an effortless monopoly.

2. SPACE: PROVEN LEADERSHIP AND AN EXPENSIVE FUTURE

The Space segment includes launch services, Dragon spacecraft, government missions and the development of Starship.

It generated approximately:

$4.09 billion in revenue during 2025

an operating loss of $657 million

segment adjusted EBITDA of $653 million

The segment also spent approximately $3 billion on research and development related to Starship during 2025.[4]

Falcon 9 has already changed the economics of orbital launch. Its reusable first stage has enabled a launch cadence that competitors have struggled to match, while Dragon has made SpaceX central to American crewed space flight.

Starship represents a much larger wager.

If it achieves reliable and rapid full reusability, Starship could reduce launch costs, deploy much larger Starlink satellites, transport very heavy payloads and make entirely new commercial activities possible.

Its potential value is enormous. So is the uncertainty.

Technical success does not automatically produce economic success. Starship must become sufficiently reliable, reusable and frequently launched to justify its development costs. It must also serve markets large enough to absorb its extraordinary capacity.

Mars, point-to-point transport on Earth and large orbital data centres may eventually create value. For present valuation purposes, they remain options rather than established businesses.

3. ARTIFICIAL INTELLIGENCE AND X: THE LARGEST OPPORTUNITY AND THE LARGEST DRAIN

SpaceX acquired xAI in February 2026. The transaction also brought X, formerly Twitter, into the group because xAI had previously acquired the social-media platform.

The AI segment generated $3.20 billion in revenue in 2025, but recorded:

an operating loss of $6.36 billion

negative segment adjusted EBITDA of $1.24 billion

capital expenditure of $12.73 billion

AI therefore accounted for approximately 61 per cent of the entire group’s capital expenditure in 2025. During the first quarter of 2026 alone, the segment spent another $7.72 billion.[3]

There is an important accounting detail.

SpaceX’s historical financial statements were retrospectively recast to include xAI and X for all periods presented. This treatment was permitted because the businesses were under common control before the legal acquisition.

The losses are therefore relevant to the company that public shareholders now own. They do not, however, describe how the original rocket and Starlink businesses performed in isolation before the transaction.

X also brought a substantial debt burden into the group. When xAI acquired the social-media platform in 2025, it inherited approximately $12 billion of X-related debt, while the combined business subsequently raised at least another $5 billion.

The structure of the SpaceX acquisition allowed this debt to remain within the xAI subsidiary and avoided an immediate refinancing requirement. That provides some legal insulation for the parent company, but it does not make the debt economically irrelevant. SpaceX shareholders still own the subsidiary, while interest costs, refinancing risk and debt covenants may restrict how much of xAI’s future cash flow can ultimately benefit the wider group.[5]

xAI offers enormous optionality. It may develop valuable models, sell computing capacity and benefit from integration with Starlink, SpaceX and future orbital infrastructure. Yet it competes against some of the best-capitalised companies in history, including Microsoft, Alphabet, Amazon, Meta, OpenAI and Anthropic.

SpaceX’s underwriters reportedly circulated projections in which AI revenue rises from $3.2 billion in 2025 to $322 billion in 2030, while total group revenue reaches $474 billion. That would require compound annual growth of approximately 151 per cent in AI revenue and 91 per cent in total group revenue over five years.[6]

These forecasts are price-relevant because they may have influenced demand for the offering. They should not be treated as independent evidence. The banks producing them were also helping to sell the IPO.

AMAZON LEO IS A MARGIN THREAT, NOT YET AN EXISTENTIAL THREAT

Starlink’s most credible direct competitor is Amazon Leo, previously known as Project Kuiper.

Amazon had deployed more than 330 satellites by early June 2026 and plans to accelerate production and launches as it approaches its initial commercial rollout. It also possesses advantages that smaller competitors cannot match:

access to Amazon’s capital

integration with Amazon Web Services

extensive relationships with companies and public authorities

global distribution and logistics

the ability to bundle cloud computing and connectivity

Amazon Leo remains far behind Starlink in satellite numbers, coverage, subscriber scale and operational experience. It also relies heavily on external launch providers, while SpaceX controls its own launch system.

It is therefore premature to describe Amazon as an existential threat to Starlink.

That does not make it irrelevant.

Amazon does not need to defeat Starlink to damage SpaceX’s valuation. It only needs to compete effectively for profitable customers, place pressure on prices or force SpaceX to invest more heavily to defend its lead.

In June 2026, the US Federal Communications Commission waived part of Amazon’s interim deployment requirement. The decision confirmed that Amazon was behind its original deployment schedule, but it also reduced the risk that the remaining constellation would be prevented from launching. Undeployed satellites face temporary consequences concerning spectrum priority, while Amazon retains a final deployment deadline in July 2029.[7]

The regulatory decision therefore has two effects at once:

it documents a significant delay

it makes Amazon’s eventual emergence as a large competitor more likely

Amazon Leo is best understood as a future constraint on Starlink’s pricing power and margins, rather than an immediate threat to its existence.

AN ILLUSTRATIVE SUM-OF-THE-PARTS VALUATION

SpaceX cannot be valued responsibly through one conventional multiple.

Starlink is a profitable infrastructure business. The existing launch operation is a strategic aerospace platform. Starship is a high-risk technological option. xAI is an early-stage AI company with enormous investment requirements. X adds commercial potential, but also financial, regulatory, reputational and governance risks.

A sum-of-the-parts analysis can help reveal what investors are paying for, but it cannot produce a scientifically precise fair value.

The following table is therefore an illustrative scenario framework, not a price target:

Even the optimistic scenario is highly generous.

It assigns Starlink a valuation of approximately 66 times its 2025 segment adjusted EBITDA. It gives hundreds of billions of dollars to Starship and the launch business despite present operating losses. It also values xAI and X at $450 billion despite AI-segment revenue of only $3.2 billion, an operating loss exceeding $6 billion and a substantial debt burden within the subsidiary.

Yet the optimistic scenario still falls below the $135 issue price.

This does not prove that $135 is wrong. It demonstrates that the valuation requires assumptions even more ambitious than those contained in an already optimistic scenario.

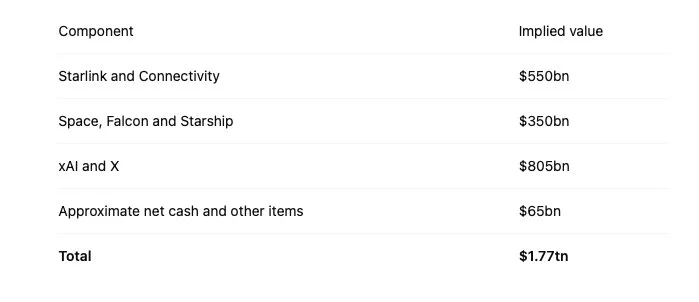

WHAT MUST BE TRUE FOR $135 TO MAKE SENSE?

A possible allocation of the $1.77 trillion valuation might look like this:

This would value:

Starlink at approximately 77 times 2025 adjusted EBITDA

the Space segment at approximately 86 times 2025 revenue

xAI and X at more than 250 times 2025 AI revenue

The allocation is not unique. More value could be assigned to Starlink and less to xAI, or the reverse.

The underlying difficulty remains the same. At least two of the three principal businesses must receive extremely aggressive valuations simultaneously.

A useful control point is the February 2026 transaction through which SpaceX acquired xAI. That transaction valued the original SpaceX business at approximately $1 trillion and xAI at $250 billion, giving a combined value of $1.25 trillion.[8]

Because both companies were controlled by Elon Musk, this was not a fully independent market transaction. It should not be treated as objective fair value.

Even so, the IPO valuation is approximately 42 per cent higher only four months later. After allowing for the new capital raised, the increase remains substantial. Publicly available financial information does not show an equivalent improvement in underlying cash generation during that short period.

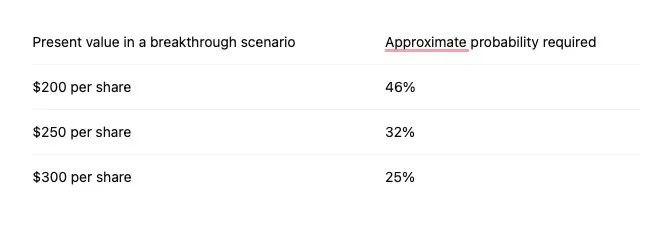

HOW MUCH PROBABILITY MUST BE ASSIGNED TO A BREAKTHROUGH?

The valuation debate can be made more precise by asking a different question:

What probability of an extraordinary breakthrough scenario is required to justify paying $135 today?

Assume, purely for illustration, that a more conventional outcome has a present value of approximately $80 per share. The following table shows the probability that must be assigned to different breakthrough values for the expected value to equal $135:

This is a deliberately simplified model.

The $80 figure is not a definitive fair-value estimate. It is a rounded analytical anchor derived from the central sum-of-the-parts scenario. Real outcomes exist on a continuum rather than in only two states. Starlink may outperform while xAI disappoints. Starship may succeed technically without generating exceptional profits. Amazon Leo may reduce margins without stopping subscriber growth.

All scenario values must also be understood as present values calculated under a consistent required return. A share price of $300 ten years from now is not the same as a present value of $300 today.

The table nevertheless clarifies the disagreement.

A rational buyer at $135 does not merely need to believe that a spectacular outcome is possible. The buyer must assign a substantial probability to a future in which several ambitious projects create exceptional economic value.

That judgement may ultimately prove correct. It is far more demanding than simply believing that SpaceX will remain an excellent company.

THE MUSK PREMIUM HAS TWO SIDES

Elon Musk’s record deserves recognition.

SpaceX achieved developments that established aerospace companies and public authorities had struggled to deliver. Reusable orbital rockets, commercial crew transport and a global satellite broadband network are not marketing concepts. They are operational achievements.

That record can justify an execution premium.

It also creates risks.

Musk controls approximately 82.4 per cent of the company’s voting power after the offering. SpaceX is consequently a controlled company under stock-exchange rules, giving ordinary shareholders limited influence over board composition, capital allocation and related-party transactions.[9]

The “Musk premium” should therefore be divided into several components:

an execution premium based on previous achievements

a founder premium based on access to capital and talent

a sentiment premium based on investor enthusiasm

a governance discount reflecting concentrated control

a key-person discount reflecting dependence on one individual

It is not analytically sufficient to argue that Musk is wealthy and has succeeded before. Successful founders can create exceptional companies and still sell shares at prices that leave future investors with poor returns.

INDEX DEMAND AND INSIDER SELLING

SpaceX is likely to enter several major indices unusually quickly. Passive funds tracking those indices may therefore be required to buy the shares.

This can create technical demand, particularly because only a relatively small percentage of the company is initially available for public trading.

Passive demand should not be confused with fundamental value. Index inclusion changes who must buy the shares. It does not change the cash flows generated by the business.

The supply side also deserves attention.

Rather than imposing one conventional 180-day insider lock-up, SpaceX created a staged structure with shares becoming eligible for sale at multiple points. Reuters reported that different tranches could be released across 16 dates, with some sales potentially permitted after early post-IPO financial results.[10]

The structure may prevent one enormous wave of insider selling. It could instead produce a prolonged increase in available shares.

The eventual effect will depend on whether new demand from index funds and retail investors is sufficient to absorb that supply.

WHEN WOULD THE SHARES BECOME MORE ATTRACTIVE?

A single fair-value estimate would suggest more certainty than the evidence allows. Decision zones are more useful.

ABOVE $120

The valuation already assumes extensive success across Starlink, Starship and artificial intelligence. The margin of safety appears extremely limited.

At this level, the shares are difficult to justify as a conventional long-term investment based on current fundamentals.

BETWEEN $90 AND $120

The valuation remains demanding. A small speculative position could be defensible for an investor with unusually strong confidence in SpaceX’s execution and the ability to tolerate severe volatility.

Such a decision would require evidence that:

Starlink continues to grow rapidly

Connectivity margins remain strong

xAI’s revenue begins to rise faster than its losses

Starship achieves significant technical and operational milestones

dilution remains under control

BETWEEN $65 AND $90

The risk-reward relationship becomes more interesting, provided that a lower price reflects reduced IPO enthusiasm rather than a fundamental deterioration in the company.

Within this range, SpaceX could become more defensible as a small satellite position alongside a broadly diversified core portfolio.

BELOW APPROXIMATELY $65

The shares would merit a complete fresh analysis.

A lower price would not automatically make SpaceX cheap. It could reflect serious problems involving Starship, Starlink competition, AI economics, governance or capital requirements.

It would, however, provide substantially more room for disappointment than the IPO valuation.

These zones are not promises, targets or trading signals. They indicate how the required margin of safety changes at different valuations.

WHAT INVESTORS SHOULD MONITOR

The investment case should be revised continually as public results become available. Three developments matter more than all others.

1. STARLINK ECONOMICS

Starlink is the only segment currently producing substantial operating profits. Subscriber growth alone is therefore insufficient. Revenue per user, operating margins, customer retention, terminal subsidies and capital expenditure per additional unit of network capacity will show whether growth is creating durable value.

2. XAI’S COMMERCIAL PROGRESS AND CASH CONSUMPTION

AI revenue must eventually grow faster than operating losses and capital expenditure. Investors should examine how much revenue comes from independent external customers, whether computing infrastructure is being used efficiently and how much additional capital xAI requires before approaching sustainable profitability.

The subsidiary’s debt burden also deserves close attention. Rising interest costs, refinancing requirements or restrictive covenants could reduce the proportion of future cash flow available to the wider SpaceX group.

3. STARSHIP EXECUTION

Starship is central to several of the assumptions embedded in SpaceX’s valuation. The most important milestones include reliable orbital operations, rapid reusability, payload deployment, orbital refuelling, launch frequency and evidence of commercial demand beyond SpaceX’s own satellite programme.

Four additional factors could materially alter the investment case.

COMPETITION FROM AMAZON LEO

The key question is not whether Amazon overtakes Starlink immediately. It is whether Amazon begins to win high-value corporate, aviation, maritime or government customers and thereby weakens Starlink’s long-term pricing power.

CAPITAL ALLOCATION

Starlink’s profits may finance projects capable of creating enormous value. They may also be consumed by ventures with uncertain returns. Public shareholders must evaluate whether profitable divisions are being used to maximise value per share or to finance a wider corporate vision.

DILUTION AND INSIDER SALES

Employee compensation, options, restricted shares, acquisitions funded with equity and staged lock-up releases may cause growth in the company’s total value to exceed growth in value per existing share.

GOVERNANCE

Related-party transactions, the integration of Musk-controlled companies and the limited influence of Class A shareholders deserve continued scrutiny.

CONCLUSION: ADMIRATION IS NOT A VALUATION METHOD

SpaceX may become one of the most important companies of the twenty-first century.

Starlink is already a powerful and profitable communications platform. Falcon has transformed orbital launch. Starship could alter the economics of access to space again. xAI may eventually create a valuable bridge between communications, computing and orbital infrastructure.

None of this means that every price is attractive.

At $135 per share, investors are paying not only for SpaceX’s existing achievements but also for a significant portion of its most ambitious future. Starlink must continue to grow without suffering excessive pressure on prices or margins. Starship must become operationally and commercially successful. xAI must turn immense capital expenditure into equally immense revenue. These developments must occur without excessive dilution, governance failures, unsustainable debt or prolonged destruction of cash.

The rational choice is not limited to enthusiasm or rejection.

A third position is available:

RECOGNISE SPACEX AS AN EXCEPTIONAL COMPANY, REMAIN SCEPTICAL OF AN EXCEPTIONALLY DEMANDING VALUATION, AND TREAT PATIENCE AS AN ACTIVE INVESTMENT DECISION.

Waiting does not imply a lack of belief in SpaceX. It means requiring either a lower price or stronger evidence that the company’s fundamentals are catching up with the expectations already embedded in the shares.

That distinction is what separates investment analysis from both hype and cynicism.

SOURCES AND METHODOLOGICAL NOTES

[1] SpaceX IPO pricing and offering information, Reuters, 11 June 2026; SpaceX Form S-1 and subsequent amendments filed with the US Securities and Exchange Commission.

[2] SpaceX, Form S-1; Reuters, “SpaceX by the Numbers: Six Charts Mapping the Businesses Driving the Largest-Ever IPO”, 11 June 2026.

[3] SpaceX, Form S-1, consolidated cash-flow and segment capital-expenditure statements; Reuters reporting on SpaceX’s AI investment and cash requirements.

[4] SpaceX, Form S-1, segment disclosures for the year ended 31 December 2025.

[5] Reuters reporting on the debt structure associated with X, xAI and the SpaceX acquisition, February 2026.

[6] Goldman Sachs projections reported by the Financial Times and Reuters. The projections were not independently verified by Reuters and should be treated as an optimistic underwriter scenario rather than a neutral forecast.

[7] Amazon corporate disclosures on Amazon Leo deployment; Federal Communications Commission, Order DA 26-553, June 2026.

[8] Reuters reporting on the February 2026 SpaceX-xAI transaction, which valued SpaceX at approximately $1 trillion and xAI at approximately $250 billion.

[9] SpaceX, Form S-1; Reuters reporting on SpaceX’s controlled-company status and shareholder rights.

[10] SpaceX IPO filings; Reuters reporting on the company’s staged post-IPO lock-up arrangements.

Disclaimer: This article is an independent analytical assessment provided for informational purposes. It does not constitute personalised investment advice or a recommendation to buy, hold or sell any security.