SPACEX AND THE PRICE OF THE FUTURE

SPACEX CLOSES AT $201.80: A HISTORIC COMPANY AT A PRICE THAT DEMANDS PERFECTION

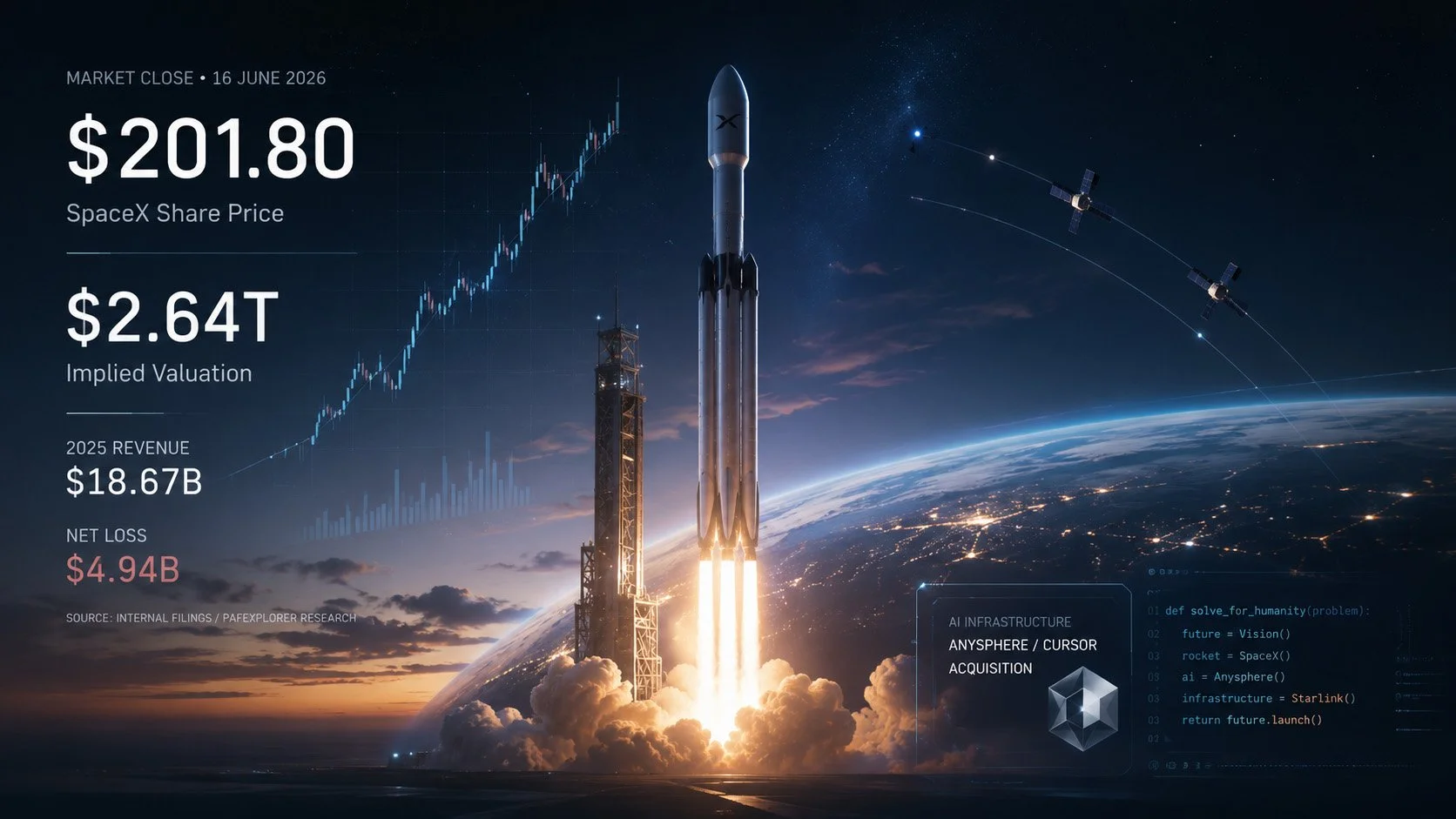

16 June 2026

Text by Max

Disclaimer: This article is an independent analytical assessment provided for informational purposes. It does not constitute personalised investment advice or a recommendation to buy, hold or sell any security.

After the largest IPO in history and a $60 billion AI acquisition, SpaceX has become one of the world’s most valuable companies. But the gap between its current business and its market value is now almost as extraordinary as the company itself.

SpaceX closed on Tuesday at $201.80, up 4.83% on the day and roughly 49.5% above its $135 IPO price, giving Elon Musk’s newly listed space, satellite broadband and AI company an implied market value of approximately $2.64 trillion.

If the additional shares sold through the IPO’s greenshoe option are included in the share count, the implied market value is closer to $2.66 trillion. Either way, the conclusion is the same: public investors are now valuing SpaceX at a level normally reserved for the largest technology companies in the world.

The move was not a one-day event. SpaceX opened at $150 on Friday, closed its first trading day at $160.95, had a previous close of $192.50 before Tuesday’s session, and then added another 4.83% to finish at $201.80.

That sequence has turned what was already the largest IPO in history into one of the most spectacular public-market debuts of the decade.

According to Reuters, SpaceX priced its initial public offering at $135 per share, raised $75 billion through the sale of 555.56 million shares, and entered the public market with a valuation of $1.77 trillion based on 13.08 billion shares outstanding. On Monday, SpaceX said its underwriters had exercised the greenshoe option, increasing total IPO proceeds to $85.7 billion.

On Tuesday, the rally was reinforced by SpaceX’s announcement that it will acquire Anysphere, the company behind the AI coding tool Cursor, in an all-stock deal worth $60 billion.

The result is a valuation that no longer reflects only rockets and satellites. SpaceX is now being priced as a possible twenty-first-century infrastructure giant, spanning launch services, satellite broadband, defence-related space systems, artificial intelligence tools and perhaps, eventually, computing infrastructure in orbit.

That may prove to be the right long-term vision. But the price already assumes a great deal of it will come true.

Key figures

Tuesday close: $201.80, up 4.83% on the day

Previous close: $192.50

IPO price: $135 per share

First trading price: $150 per share

First-day close: $160.95

Gain from IPO price to Tuesday close: approximately 49.5%

Implied market value at Tuesday close: approximately $2.64 trillion using Reuters’ IPO share count of 13.08 billion shares, or about $2.66 trillion if the additional greenshoe shares are included

2025 revenue: $18.67 billion

2025 net loss: $4.94 billion

Sales multiple at Tuesday close: roughly 141 to 142 times 2025 revenue

Revenue behind each $100 of market value: roughly 70 to 71 cents

Anysphere/Cursor acquisition: $60 billion, paid in SpaceX shares

Starlink users: about 10.3 million, according to Reuters reporting

Sources for key figures: market close data and Reuters reporting on SpaceX’s IPO, financials, first trading day, greenshoe option, Anysphere transaction, options trading and Starlink user growth.

The $100 and roughly 70 cents problem

At Tuesday’s closing price of $201.80, SpaceX is worth approximately $2.64 trillion, or around $2.66 trillion if the additional greenshoe shares are included. Against 2025 revenue of $18.67 billion, that means the stock is trading at roughly 141 to 142 times annual revenue.

Put more plainly: for every $100 of market value, SpaceX generated only about 70 to 71 cents of revenue in 2025.

That is not the same as saying SpaceX is “really worth” 70 cents for every $100. Revenue is not intrinsic value. A company can be worth many times its current sales if future profits are expected to be enormous.

But the comparison is a useful reality check.

It shows that today’s share price is not mainly about what SpaceX earned last year. It is about what investors believe SpaceX could become over the next decade or more. The market is not buying a conventional aerospace company. It is buying a story about future dominance across space, broadband, AI and strategic infrastructure.

That story may prove right. But it leaves little room for disappointment.

A remarkable company, not a cheap stock

SpaceX is not a hollow market bubble. It has reshaped the economics of space launch through reusable rockets. Falcon 9 has become the workhorse of the global launch market. Starlink has turned low-Earth-orbit satellite broadband into a real commercial business. SpaceX is also deeply embedded in US government, defence and national security space infrastructure.

These are not imaginary assets. They are real businesses with real customers, real technology and strategic importance.

That is what makes SpaceX different from many speculative growth stories. The company has already achieved what others have only promised.

But the stock market is now valuing more than those achievements. It is valuing the possibility that SpaceX becomes a dominant infrastructure platform, not only for space access and satellite communications, but also for AI and computing.

That is a much larger claim.

In 2025, SpaceX generated $18.67 billion in revenue but posted a net loss of $4.94 billion. The 2025 loss should not automatically be treated as proof that the business model is weak. Reuters has reported that aggressive spending on computing power for AI and the development of new rocket systems has weighed heavily on the company’s financials, even as Starlink has grown rapidly.

But at a valuation above $2.6 trillion, investors need more than ambition. They need evidence that today’s investment can eventually become durable profit.

Why the stock is rising

Tuesday’s move was not driven by one factor alone.

Part of the rally reflects scarcity. For years, SpaceX was one of the world’s most desired private companies, but direct exposure was largely limited to private investors, employees and selected institutions. The IPO opened the door to public-market demand that had been building for a long time.

Part of it reflects momentum. Once a newly listed mega-cap stock rises sharply, traders, funds and options markets can amplify the move.

Options trading added another layer of momentum. Reuters reported that around 1.3 million SpaceX options contractshad changed hands by 2 p.m. ET on Tuesday, with call options outpacing puts. That matters because heavy call buying can force market makers to buy the underlying shares to hedge their own risk, potentially amplifying a rally in the stock itself.

This does not mean the rise is artificial. But it does mean that part of Tuesday’s move may have been driven by market mechanics as well as by long-term conviction in SpaceX’s business.

Part of the rally also reflects possible index demand. Reuters has reported that index inclusion is one of the near-term events investors are watching after the IPO. If SpaceX is added to major indices, some passive funds and ETFs may be forced to buy the stock mechanically, regardless of whether they consider the valuation attractive.

The S&P 500 is different. A swift entry into that index may be harder because of rules around profitability, trading history and public float. That distinction matters: index demand may support the shares, but not all major index demand arrives at once.

And part of the rally reflects the Musk factor. Investors are paying for Elon Musk’s record of turning implausible engineering ambitions into dominant businesses. Tesla changed the car industry. SpaceX changed the launch industry. Starlink changed satellite broadband.

That record is real. So is the risk of overpaying for it.

The Anysphere deal changes the investment case

The proposed acquisition of Anysphere, the company behind Cursor, is more than an ordinary technology deal.

It moves SpaceX further into artificial intelligence and strengthens the case that investors should not view the company as a pure space business. Cursor is one of the most visible AI coding tools and gives SpaceX and xAI a stronger position in a part of the AI market where customers have already shown willingness to pay for productivity gains.

But the deal also shows how powerful SpaceX’s share price has become as a financial instrument.

Because the Anysphere acquisition is being paid in SpaceX stock at current market prices, a high share price allows the company to buy strategic assets with relatively limited dilution. That can be intelligent capital allocation if the acquired business strengthens the long-term platform. It can also become dangerous if the stock later falls and the transaction looks expensive in hindsight.

In that sense, the Anysphere deal is both a sign of strength and a warning. SpaceX can now use its valuation to expand. But the higher the valuation climbs, the more carefully investors should ask whether each deal creates real long-term value or simply uses expensive shares while the market is enthusiastic.

AI is still the least proven part of the story

SpaceX’s strongest proven businesses are launch and Starlink. The most speculative part of the valuation is AI.

xAI gives SpaceX exposure to one of the largest technology markets in the world, and Cursor adds a serious software product in AI-assisted coding. But SpaceX is competing against OpenAI, Anthropic, Google and other companies with enormous resources, strong models and deep enterprise relationships.

The Anysphere deal narrows a gap. It does not automatically close it.

Investors therefore have to decide whether SpaceX deserves to be valued as a future AI infrastructure giant, or whether the market is attaching too much value to ambitions that are still difficult to measure.

That question matters because SpaceX has presented artificial intelligence and space-based computing as central parts of its long-term growth story. The idea is bold: if Earth-based data centres face limits from power, land and permitting, orbital infrastructure could one day offer a different path. But that remains an ambition, not a mature business.

The share price is already giving SpaceX significant credit for that ambition.

Competition has not disappeared

SpaceX is the clear leader in many parts of the space economy, but it is not without competitors.

In launch, Rocket Lab remains a serious public-market space company, particularly in small launch and its planned medium-lift Neutron rocket. Blue Origin remains a long-term rival backed by Jeff Bezos, even after delays and setbacks. United Launch Alliance, Arianespace and newer players such as Stoke Space also matter, especially for government, defence and specialised launch contracts.

In satellite broadband, Starlink has a large lead, but Amazon Leo, formerly Project Kuiper, is a serious future competitor. Amazon has capital, cloud infrastructure, enterprise customers and a strategic reason to challenge SpaceX in low-Earth-orbit communications. Eutelsat OneWeb and Europe’s future IRIS2 project also show that governments and telecom groups do not want one private American company to control the future of satellite connectivity.

SpaceX may remain the leader. But a valuation above $2.6 trillion assumes that leadership can be defended for many years in several markets at once.

Musk control cuts both ways

Elon Musk is central to the investment case. That is both the premium and the risk.

Reuters has reported that Musk retains overwhelming voting control at SpaceX and that the company’s governance structure gives outside shareholders limited influence. For investors, that creates a clear trade-off.

On one hand, concentrated control can protect long-term strategy. SpaceX can pursue ambitious projects without constantly responding to short-term shareholder pressure.

On the other hand, public investors are buying economic exposure without meaningful control. If they disagree with acquisitions, governance, strategy, related-party decisions or risk-taking, their ability to influence the company is limited.

That does not make SpaceX uninvestable. It does mean investors need to understand what they are buying.

They are not buying a conventional public company with conventional shareholder power. They are buying into Elon Musk’s controlled technology empire.

A short timeline

June 11: SpaceX prices its IPO at $135 per share, raising $75 billion and valuing the company at $1.77 trillion.

June 12: SpaceX begins trading on Nasdaq. The stock opens at $150 and closes at $160.95, giving the company a valuation above $2 trillion.

June 15: SpaceX’s previous close stood at about $192.50. Separately, the company said underwriters had exercised the greenshoe option, increasing total IPO proceeds to $85.7 billion.

June 16: SpaceX announces a $60 billion all-stock deal to acquire Anysphere, the company behind Cursor.

June 16: SpaceX options begin trading with exceptionally heavy volume, adding another source of momentum and volatility.

After market close, June 16: SpaceX closes at $201.80, implying a market value of approximately $2.64 trillion, or about $2.66 trillion if the additional greenshoe shares are included.

Conclusion: extraordinary company, extraordinary expectations

SpaceX may be one of the most important technology companies of the modern era. Its rockets have lowered launch costs, Starlink has built the world’s leading satellite broadband network, and its ambitions in AI and orbital infrastructure could reshape more than one industry.

But the valuation is already pricing in a very large part of that future.

At $201.80 per share, investors are paying roughly $100 in market value for every 70 to 71 cents of 2025 revenue. They are also paying that price for a company that lost nearly $5 billion last year.

That does not make SpaceX a bad company. It makes the stock a demanding one.

For long-term believers, SpaceX may still be a once-in-a-generation platform. For valuation-focused investors, it is a reminder that even extraordinary companies can become extremely expensive when the market starts paying for the future before it has arrived.

This article is for news and analysis only and does not constitute investment advice.

Main sources: Reuters reporting on SpaceX’s IPO, market debut, financials, greenshoe option, options trading, index outlook and Anysphere/Cursor transaction; market close data for SPCX on 16 June 2026.